📖 Dynamic Programming#

⏱ | words

What is dynamic programming?#

“DP is recursive method for solving sequential decision problems”

📖 Rust 2006, New Palgrave Dictionary of Economics

In computer science the meaning of the term is broader: DP is a general algorithm design technique for solving problems with overlapping sub-problems.

Dynamic programming in economics#

DP provides a framework to study decision making over time and under uncertainty and can accommodate learning, strategic interactions between agents (game theory) and market interactions (equilibrium theory)

Many important problems and economic models are analyzed and solved using dynamic programming:

Dynamic models of labor supply

Job search

Human capital accumulation

Health process, insurance and long term care

Consumption/savings choices

Durable consumption

Growth models

Heterogeneous agents models

Overlapping generation models

Dynamic discrete choice (DDC)#

Extend the discrete choice framework to repeated discrete choice over time

Given state \(s_t \in S\) an agent takes a decision \(d_t \in D(s)\) that determines current utility \(u_t(s_t,d_t)\) as well as the future states of the world.

The agent forms (subjective) beliefs about the uncertain next period’s state \(s_{t+1}\) that evolve according to a Markov transition probability \(p(s_{t+1}|s_t, d_t)\).

The agent’s problem is to choose a optimal decision rule \(\mathbf{\delta} = \{\delta_0,...,\delta_T\}\), where \(d_t=\delta_t(s_t)\), that solves

where \(\mathbb{E}_{\delta}\) denotes expectation with respect to the controlled stochastic process \(\{s_t,d_t\}\) induced by the decision rule \(\delta\).

The difficulty is that we are looking for a set of functions \(\mathbf{\delta} = \{\delta_0,...,\delta_T\}\), not just for a set of numbers \(\mathbf{d} = \{d_0,...,d_T\}\)

DP simplifies the DDC problem, allowing us to find \(\mathbf{\delta} = \{\delta_0,...,\delta_T\}\) using a recursive procedure.

Bellman’s Principle of Optimality#

An optimal policy has a property that whatever the initial state and initial decision are, the remaining decisions must constitute an optimal policy with regard to the state resulting from the first decision.

📖 Bellman, 1957 “Dynamic Programming”

Breaking the problem into sequence of small problems#

Thus, the sequential decision problem is broken into initial decision problem and the future decisions problem

The solution can be computed through backward induction, i.e. solving a sequential decision problem from the later periods

Embodiment of the recursive way of modeling sequential decisions is Bellman equation

Bellman equation#

Definition

Bellman equation is the complete recursive description of the dynamic optimization problem in discrete time:

State variables — vector of variables that describe all relevant information about the modeled decision process, \(x_t\)

Decision variables — vector of variables describing the choices, \(d_t\)

Instantaneous payoff — utility function, \(u(x_t,d_t)\), with time separable discounted utility

(next state) is the stochastic next period state resulting from current state and decision

expectation \(\mathbb{E}\{\cdot\}\) is taken over the distribution of the next period state conditional on current state and decision

Motion rules — agent’s beliefs of how state variable evolve through time, conditional on choices, \(x_{t+1} \sim F(x_t,d_t)\)

\(\beta\) is a discount factor to measure future rewards in terms of current ones

Solution is given by:

Value function — maximum attainable utility \(V(x_t)\)

Policy function — mapping from state space to action space that returns the optimal choice, \(d^{\star}(x_t)\)

The optimal choices are revealed along the solution of the Bellman equation as decisions which solve the maximization problem in the right hand side (\(\arg\max\) of the maximization in the Bellman equation)

Classification of DP models#

Discrete or continuous time?

Finite or infinite horizon?

Choice space (discrete, continuous, mixed)?

State space (finite, discretized)?

Stochastic or deterministic evolution of states?

Whether choice is part of the problem at all#

Computer science uses DP to solve problems without explicit decisions, but breaking big problems into a series of small ones lecture 27 in CompEcon course

Examples of sequential discrete/discretized choice

deal or no deal problem lecture 27 in CompEcon course

inventory management model (see below)

Rust model of bus engine replacement lecture 28, 29 in CompEcon course

cake eating problem lecture 30, 32 in CompEcon course

consumption-savings problem lecture 35 in CompEcon course

Whether choice space is discrete, continuous, mixed discrete-continuous or discretized#

Problems with discrete choice

deal or no deal problem, inventory management model lecture 27 in CompEcon course

Rust model of bus engine replacement lectures 28, 29 in CompEcon course

Problems with continuous choice

discretized: cake eating problem lecture 30 in CompEcon course , consumption-savings models lecture 35 in CompEcon course

treated as continuous: coming up next

require interpolating of value function in Bellman equation

Problems with discrete and continuous choice

much more complicated: kinks in value functions, discontinuous policy function

require global optimization in Bellman equation which is not easy

one way out is to discretize choices at the cost of reduced accuracy

see our paper Iskhakov et al. [2017] for how to smooth the kinks

What about state space?#

When choice is discrete, typically state space is also finite

Even when state variables are continuous, by discretization it is converted to discrete

This is true in general when using numerical solvers: state space is discretized within some reasonable bounds

choice of upper bounds, number and placement of grid points influence the (accuracy of the) solution

Another approach to represent state space is to project value and/or policy function onto space of orthogonal polynomials (Chebyshev polynomials in particular)

only works well when value function is sufficiently smooth

Whether time is continuous or discrete#

Discrete time

time periods \(t\), \(t+1\)

dynamics given by difference equations

Continuous time

all entities in the model are functions of time

dynamics given by differential equation

so, math is very different

continuous time for cleaner theoretical models, sometimes also solved numerically

not part of this course

Whether horizon is finite or infinite#

Finite horizon

there is terminal period \(T\)

special form of Bellman equation in period \(T\)

in other words, as if \(V(\text{at } T +1 ) = \mathbb{0}\)

value function and policy function are time dependent

solved by backwards induction with \(T\) number of steps

Infinite horizon

time subscripts are dropped, primes for next period values instead

solution is given by fixed point of the Bellman operator

have to actually solve a functional equation

Most problems can be specified and solved in both finite or infinite horizon

Whether model includes stochastic processes#

Deterministic models

No random elements, all motion rules deterministic

No need for expectation operator in Bellman equation

Stochastic models with idiosyncratic shocks

expectation does not have to be conditioned on current period shocks

solving the fixed point in expected value function space is beneficial

General form stochastic models

expectation in Bellman equation has to be computed with quadrature or Monte Carlo integration

Example: Inventory management model#

Consider the following problem in discrete time and finite horizon \(t=0,\dots,T\)

The notation is:

\(x_t\ge 0\) is inventory at period \(t\) measured in discrete units

\(d_t\ge 0\) is potentially stochastic demand at period \(t\)

\(q_t\ge 0\) is the order of new inventory

\(p\) is the profit per one unit of (supplied) good

\(c\) is the fixed cost of ordering any amount of new inventory

\(r\) is the cost of storing one unit of good

The sales in period \(t\) are given by \(s_t = \min\{x_t,d_t\}\).

Inventory to be stored till next period is given by \(k_t = \max\{x_t-d_t,0\} + q_t = x_{t+1}\).

The profit in period \(t\) is given by

Assuming all \(q_t \ge 0\), let \(\sigma = \{q_t\}_{t=1,\dots,T}\) denote a feasible inventory policy.

If \(d_t\) is stochastic the policy becomes a function of the period \(t\) inventory \(x_t\).

The expected profit maximizing problem is given by

where \(\beta\) is discount factor.

Bellman equation for the problem#

Decisions: \(q_t\), how much new inventory to order

What is important for the inventory decision at time period \(t\)?

instanteneous utility (profit) contains \(x_t\) and \(d_t\)

timing / sequence of events:

(beginning of period)

current inventory

demand

order (choice)

stored inventory

(end of period)

So, both \(x_t\) and \(d_t\) are taken into account for the new order to be made, forming the state space.

The expectation in the Bellman equation is taken over the distribution of the next period demand \(d_{t+1}\), which we assume is independent of any other variables and across time (idiosyncratic), thus the conditioning on \((x_t,d_t,s_t)\) can be meaningfully dropped.

Expectation can be written as an integral over the distribution of demand \(F(d)\), and since inventory is discrete it’s natural to assume demand is as well.

The integral then transforms into a sum over the possible value of demand, weighted by their probabilities \(pr(d)\)

But let’s focus first on a deterministic case: let \(d\) be fixed and constant over time. How does the Bellman equation change?

In the deterministic case with fixed \(d\), it can be simply dropped from the state space, and the Bellman equation can be simplified to

How does this convert to the code?

model=inventory_model(label='test')

print(model)

q=np.zeros(model.n)

print('Current profits with zero orders\n',model.profit(model.x,model.demand,q))

Inventory model labeled "test"

Paramters (c,p,r,β) = (3.2,2.5,0.5,0.95)

Demand=4

Upper bound on inventory 10

Current profits with zero orders

[ 0. 2.5 5. 7.5 10. 9.5 9. 8.5 8. 7.5 7. ]

# illustration of broadcasting in the inventory model

q=model.x[:,np.newaxis] # column vector

print('Current inventory\n',model.x)

print('Current sales\n',model.sales(model.x,model.demand))

print('Current orders\n',q)

print('Next period inventory\n',model.next_x(model.x,model.demand,q))

print('Current profits\n',model.profit(model.x,model.demand,q))

Current inventory

[ 0 1 2 3 4 5 6 7 8 9 10]

Current sales

[0 1 2 3 4 4 4 4 4 4 4]

Current orders

[[ 0]

[ 1]

[ 2]

[ 3]

[ 4]

[ 5]

[ 6]

[ 7]

[ 8]

[ 9]

[10]]

Next period inventory

[[ 0 0 0 0 0 1 2 3 4 5 6]

[ 1 1 1 1 1 2 3 4 5 6 7]

[ 2 2 2 2 2 3 4 5 6 7 8]

[ 3 3 3 3 3 4 5 6 7 8 9]

[ 4 4 4 4 4 5 6 7 8 9 10]

[ 5 5 5 5 5 6 7 8 9 10 11]

[ 6 6 6 6 6 7 8 9 10 11 12]

[ 7 7 7 7 7 8 9 10 11 12 13]

[ 8 8 8 8 8 9 10 11 12 13 14]

[ 9 9 9 9 9 10 11 12 13 14 15]

[10 10 10 10 10 11 12 13 14 15 16]]

Current profits

[[ 0. 2.5 5. 7.5 10. 9.5 9. 8.5 8. 7.5 7. ]

[-3.7 -1.2 1.3 3.8 6.3 5.8 5.3 4.8 4.3 3.8 3.3]

[-4.2 -1.7 0.8 3.3 5.8 5.3 4.8 4.3 3.8 3.3 2.8]

[-4.7 -2.2 0.3 2.8 5.3 4.8 4.3 3.8 3.3 2.8 2.3]

[-5.2 -2.7 -0.2 2.3 4.8 4.3 3.8 3.3 2.8 2.3 1.8]

[-5.7 -3.2 -0.7 1.8 4.3 3.8 3.3 2.8 2.3 1.8 1.3]

[-6.2 -3.7 -1.2 1.3 3.8 3.3 2.8 2.3 1.8 1.3 0.8]

[-6.7 -4.2 -1.7 0.8 3.3 2.8 2.3 1.8 1.3 0.8 0.3]

[-7.2 -4.7 -2.2 0.3 2.8 2.3 1.8 1.3 0.8 0.3 -0.2]

[-7.7 -5.2 -2.7 -0.2 2.3 1.8 1.3 0.8 0.3 -0.2 -0.7]

[-8.2 -5.7 -3.2 -0.7 1.8 1.3 0.8 0.3 -0.2 -0.7 -1.2]]

Backwards induction#

Backwards induction algorithm is used to solve finite horizon models

Solver for the finite horizon dynamic programming problems

1. Start at t=T

1. Solve Bellman equation at t, record optimal choice

1. Decrease t unless t=1, and return to previous step.

As result, for all t=1,..,T have found the optimal choice (as a function of state)

First, we need to code up the Bellman equation

v = np.zeros(model.n)

for i in range(3):

v,q = bellman(model,v)

print('Value =',v,'Policy =',q,sep='\n',end='\n\n')

Value =

[ 0. 2.5 5. 7.5 10. 9.5 9. 8.5 8. 7.5 7. ]

Policy =

[0 0 0 0 0 0 0 0 0 0 0]

Value =

[ 4.3 6.8 9.3 11.8 14.3 14.3 14.3 15.625 17.5 16.525

15.55 ]

Policy =

[4 4 4 4 4 3 2 0 0 0 0]

Value =

[ 9.425 11.925 14.425 16.925 19.425 19.425 19.425 19.71 21.585 21.085

20.585]

Policy =

[8 8 8 8 8 7 6 0 0 0 0]

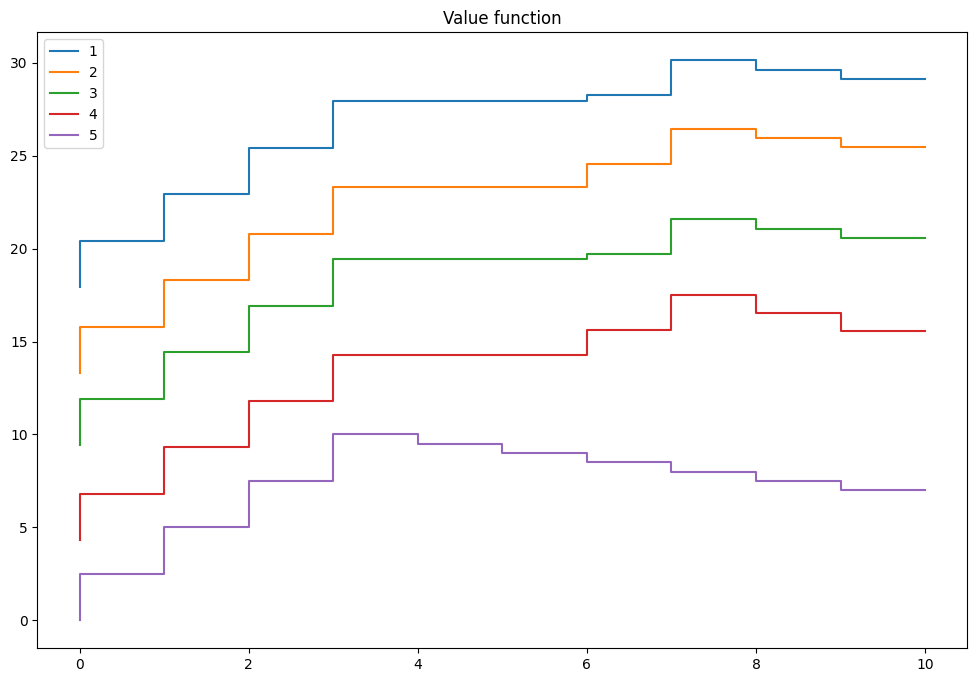

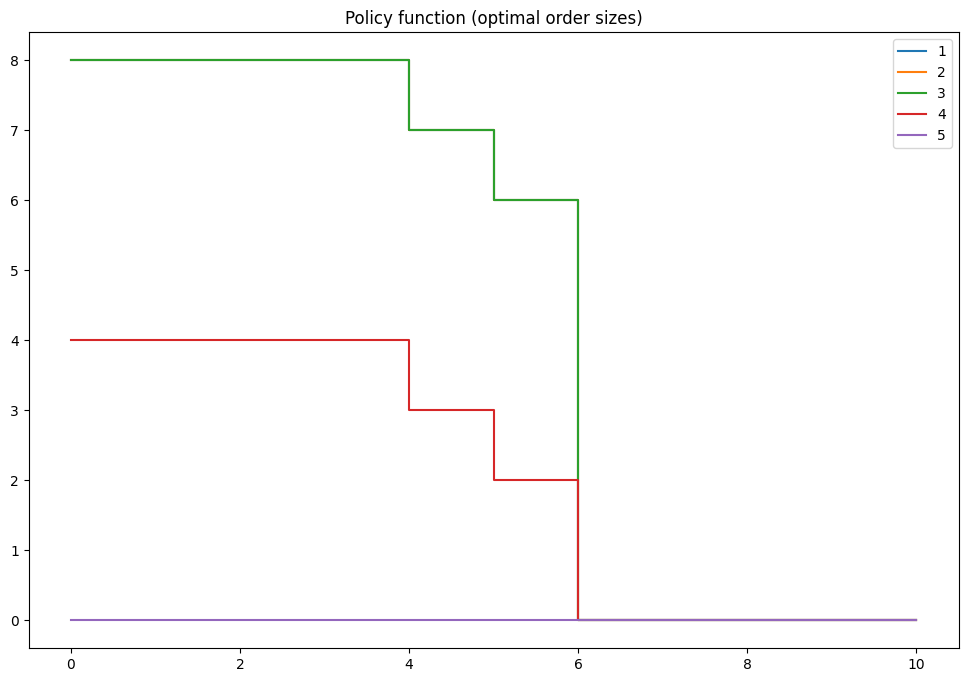

Time period 5

[[ 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 2.5]

[ 0. 0. 0. 0. 5. ]

[ 0. 0. 0. 0. 7.5]

[ 0. 0. 0. 0. 10. ]

[ 0. 0. 0. 0. 9.5]

[ 0. 0. 0. 0. 9. ]

[ 0. 0. 0. 0. 8.5]

[ 0. 0. 0. 0. 8. ]

[ 0. 0. 0. 0. 7.5]

[ 0. 0. 0. 0. 7. ]]

Time period 4

[[ 0. 0. 0. 4.3 0. ]

[ 0. 0. 0. 6.8 2.5 ]

[ 0. 0. 0. 9.3 5. ]

[ 0. 0. 0. 11.8 7.5 ]

[ 0. 0. 0. 14.3 10. ]

[ 0. 0. 0. 14.3 9.5 ]

[ 0. 0. 0. 14.3 9. ]

[ 0. 0. 0. 15.625 8.5 ]

[ 0. 0. 0. 17.5 8. ]

[ 0. 0. 0. 16.525 7.5 ]

[ 0. 0. 0. 15.55 7. ]]

Time period 3

[[ 0. 0. 9.425 4.3 0. ]

[ 0. 0. 11.925 6.8 2.5 ]

[ 0. 0. 14.425 9.3 5. ]

[ 0. 0. 16.925 11.8 7.5 ]

[ 0. 0. 19.425 14.3 10. ]

[ 0. 0. 19.425 14.3 9.5 ]

[ 0. 0. 19.425 14.3 9. ]

[ 0. 0. 19.71 15.625 8.5 ]

[ 0. 0. 21.585 17.5 8. ]

[ 0. 0. 21.085 16.525 7.5 ]

[ 0. 0. 20.585 15.55 7. ]]

Time period 2

[[ 0. 13.30575 9.425 4.3 0. ]

[ 0. 15.80575 11.925 6.8 2.5 ]

[ 0. 18.30575 14.425 9.3 5. ]

[ 0. 20.80575 16.925 11.8 7.5 ]

[ 0. 23.30575 19.425 14.3 10. ]

[ 0. 23.30575 19.425 14.3 9.5 ]

[ 0. 23.30575 19.425 14.3 9. ]

[ 0. 24.57875 19.71 15.625 8.5 ]

[ 0. 26.45375 21.585 17.5 8. ]

[ 0. 25.95375 21.085 16.525 7.5 ]

[ 0. 25.45375 20.585 15.55 7. ]]

Time period 1

[[17.9310625 13.30575 9.425 4.3 0. ]

[20.4310625 15.80575 11.925 6.8 2.5 ]

[22.9310625 18.30575 14.425 9.3 5. ]

[25.4310625 20.80575 16.925 11.8 7.5 ]

[27.9310625 23.30575 19.425 14.3 10. ]

[27.9310625 23.30575 19.425 14.3 9.5 ]

[27.9310625 23.30575 19.425 14.3 9. ]

[28.2654625 24.57875 19.71 15.625 8.5 ]

[30.1404625 26.45375 21.585 17.5 8. ]

[29.6404625 25.95375 21.085 16.525 7.5 ]

[29.1404625 25.45375 20.585 15.55 7. ]]

Optimal policy:

[[8. 8. 8. 4. 0.]

[8. 8. 8. 4. 0.]

[8. 8. 8. 4. 0.]

[8. 8. 8. 4. 0.]

[8. 8. 8. 4. 0.]

[7. 7. 7. 3. 0.]

[6. 6. 6. 2. 0.]

[0. 0. 0. 0. 0.]

[0. 0. 0. 0. 0.]

[0. 0. 0. 0. 0.]

[0. 0. 0. 0. 0.]]

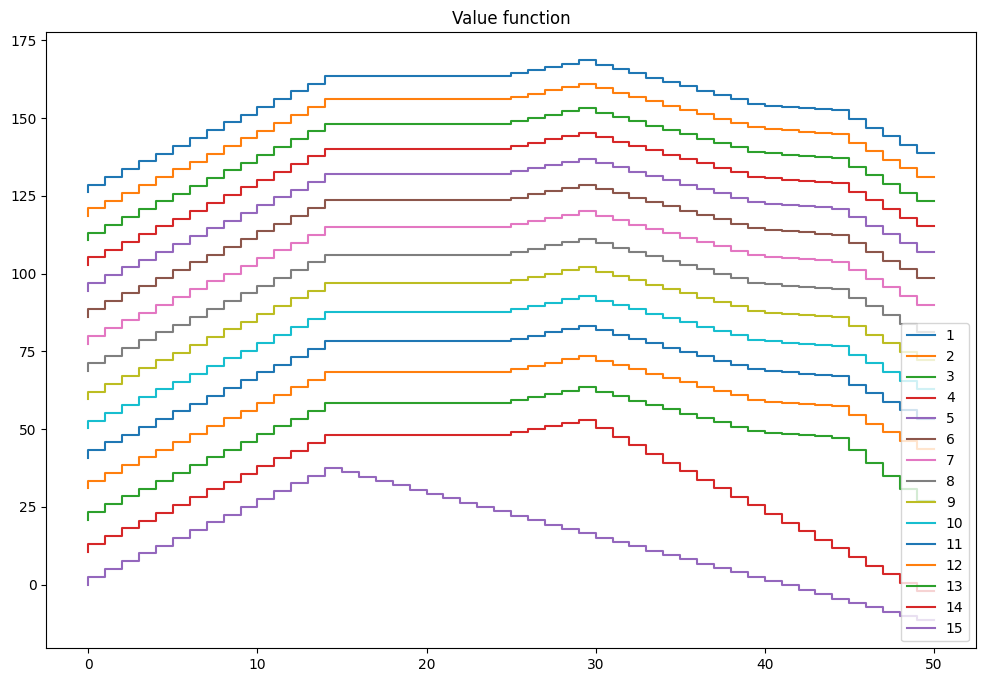

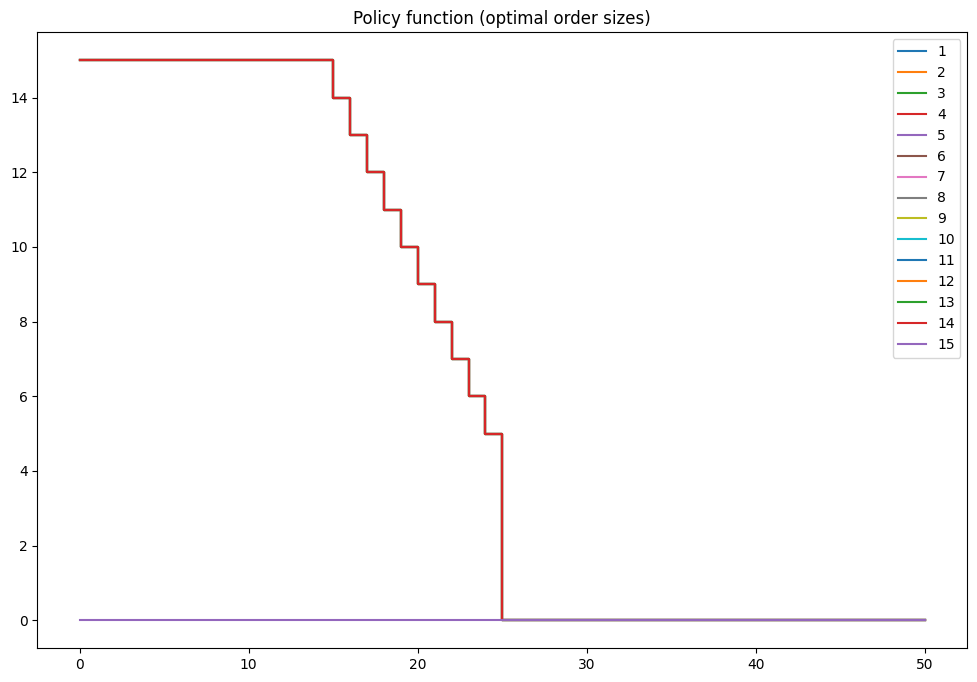

mod = inventory_model(label='production',max_inventory=50)

mod.demand = 15

mod.c = 5

mod.p = 2.5

mod.r = 1.4

mod.β = 0.975

mod = solver_backwards_induction(mod,T=15)

plot_solution(mod)

Contraction mappings and fixed points#

Solution of a dynamic model in infinite horizon is the solution to the Bellman euqation which is an actual equation in function space

We rely on contraction properties of the Bellman operator to find the fixed point that in order to solve infinite horizon dynamic models

Definition

Let

\( (S,\rho) \) be a complete metric space

\( T: S \rightarrow S \) denote an operator mapping \( S \) to itself

\( T \) is called a contraction on \( S \) with modulus \( \lambda \) if \( 0 \le \lambda < 1 \) and

Contraction mapping brings points in its domain “closer” to each other!

Example of contraction

interest rate \(r\)

What is the value of the annuity \(V\)?

Assuming \(\beta<1\)

But we can also reformulate recursively (as “Bellman equation” without choice)

contraction mapping under Euclidean norm!

modulus \(\beta\)

Successive approximations to find the value of annuity

Start with a guess \(V_0\)

Insert into the “Bellman equation”

Repeat until convergence

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

class annuity():

def __init__(self,c=1,beta=.9):

self.c = c # Annual payment

self.beta = beta # Discount factor

self.analytic = c/(1-beta) # compute analytic solution right away

def bellman(self,V):

'''Bellman equation'''

return self.c + self.beta*V

def solve(self, maxiter = 1000, tol=1e-4, verbose=False):

'''Solves the model using successive approximations'''

if verbose: print('{:<4} {:>15} {:>15}'.format('Iter','Value','Error'))

V0=0

for i in range(maxiter):

V1=self.bellman(V0)

if verbose: print('{:<4d} {:>15.8f} {:>15.8f}'.format(i,V1,V1-self.analytic))

if abs(V1-V0) < tol:

break

V0=V1

else: # when i went up to maxiter

print('No convergence: maximum number of iterations achieved!')

return V1

a = annuity(c=10,beta=0.954)

print('Analytic solution is',a.analytic)

print('Numeric solution is ',a.solve())

Analytic solution is 217.3913043478259

Numeric solution is 217.38928066546833

a.solve(verbose=True)

Iter Value Error

0 10.00000000 -207.39130435

1 19.54000000 -197.85130435

2 28.64116000 -188.75014435

3 37.32366664 -180.06763771

4 45.60677797 -171.78452637

5 53.50886619 -163.88243816

6 61.04745834 -156.34384600

7 68.23927526 -149.15202909

8 75.10026860 -142.29103575

9 81.64565624 -135.74564811

10 87.88995605 -129.50134829

11 93.84701808 -123.54428627

12 99.53005524 -117.86124910

13 104.95167270 -112.43963164

14 110.12389576 -107.26740859

15 115.05819655 -102.33310779

16 119.76551951 -97.62578484

17 124.25630562 -93.13499873

18 128.54051556 -88.85078879

19 132.62765184 -84.76365251

20 136.52677986 -80.86452449

21 140.24654798 -77.14475636

22 143.79520678 -73.59609757

23 147.18062726 -70.21067708

24 150.41031841 -66.98098594

25 153.49144376 -63.89986058

26 156.43083735 -60.96046700

27 159.23501883 -58.15628552

28 161.91020797 -55.48109638

29 164.46233840 -52.92896595

30 166.89707083 -50.49423351

31 169.21980557 -48.17149877

32 171.43569452 -45.95560983

33 173.54965257 -43.84165178

34 175.56636855 -41.82493580

35 177.49031560 -39.90098875

36 179.32576108 -38.06554327

37 181.07677607 -36.31452828

38 182.74724437 -34.64405998

39 184.34087113 -33.05043322

40 185.86119106 -31.53011329

41 187.31157627 -30.07972808

42 188.69524376 -28.69606059

43 190.01526255 -27.37604180

44 191.27456047 -26.11674388

45 192.47593069 -24.91537366

46 193.62203788 -23.76926647

47 194.71542414 -22.67588021

48 195.75851463 -21.63278972

49 196.75362295 -20.63768140

50 197.70295630 -19.68834805

51 198.60862031 -18.78268404

52 199.47262377 -17.91868057

53 200.29688308 -17.09442127

54 201.08322646 -16.30807789

55 201.83339804 -15.55790631

56 202.54906173 -14.84224262

57 203.23180489 -14.15949946

58 203.88314187 -13.50816248

59 204.50451734 -12.88678701

60 205.09730954 -12.29399481

61 205.66283330 -11.72847104

62 206.20234297 -11.18896138

63 206.71703520 -10.67426915

64 207.20805158 -10.18325277

65 207.67648120 -9.71482314

66 208.12336307 -9.26794128

67 208.54968837 -8.84161598

68 208.95640270 -8.43490165

69 209.34440818 -8.04689617

70 209.71456540 -7.67673895

71 210.06769539 -7.32360895

72 210.40458141 -6.98672294

73 210.72597066 -6.66533369

74 211.03257601 -6.35872834

75 211.32507751 -6.06622683

76 211.60412395 -5.78718040

77 211.87033425 -5.52097010

78 212.12429887 -5.26700548

79 212.36658112 -5.02472322

80 212.59771839 -4.79358596

81 212.81822335 -4.57308100

82 213.02858507 -4.36271928

83 213.22927016 -4.16203419

84 213.42072373 -3.97058062

85 213.60337044 -3.78793391

86 213.77761540 -3.61368895

87 213.94384509 -3.44745926

88 214.10242822 -3.28887613

89 214.25371652 -3.13758783

90 214.39804556 -2.99325879

91 214.53573546 -2.85556888

92 214.66709163 -2.72421272

93 214.79240542 -2.59889893

94 214.91195477 -2.47934958

95 215.02600485 -2.36529950

96 215.13480863 -2.25649572

97 215.23860743 -2.15269692

98 215.33763149 -2.05367286

99 215.43210044 -1.95920391

100 215.52222382 -1.86908053

101 215.60820152 -1.78310283

102 215.69022425 -1.70108010

103 215.76847394 -1.62283041

104 215.84312414 -1.54818021

105 215.91434043 -1.47696392

106 215.98228077 -1.40902358

107 216.04709585 -1.34420850

108 216.10892944 -1.28237491

109 216.16791869 -1.22338566

110 216.22419443 -1.16710992

111 216.27788148 -1.11342286

112 216.32909894 -1.06220541

113 216.37796038 -1.01334396

114 216.42457421 -0.96673014

115 216.46904379 -0.92226055

116 216.51146778 -0.87983657

117 216.55194026 -0.83936409

118 216.59055101 -0.80075334

119 216.62738566 -0.76391869

120 216.66252592 -0.72877843

121 216.69604973 -0.69525462

122 216.72803144 -0.66327291

123 216.75854200 -0.63276235

124 216.78764906 -0.60365528

125 216.81541721 -0.57588714

126 216.84190802 -0.54939633

127 216.86718025 -0.52412410

128 216.89128996 -0.50001439

129 216.91429062 -0.47701373

130 216.93623325 -0.45507110

131 216.95716652 -0.43413783

132 216.97713686 -0.41416749

133 216.99618856 -0.39511578

134 217.01436389 -0.37694046

135 217.03170315 -0.35960120

136 217.04824481 -0.34305954

137 217.06402555 -0.32727880

138 217.07908037 -0.31222398

139 217.09344267 -0.29786167

140 217.10714431 -0.28416004

141 217.12021567 -0.27108868

142 217.13268575 -0.25861860

143 217.14458221 -0.24672214

144 217.15593142 -0.23537292

145 217.16675858 -0.22454577

146 217.17708768 -0.21421666

147 217.18694165 -0.20436270

148 217.19634234 -0.19496201

149 217.20531059 -0.18599376

150 217.21386630 -0.17743805

151 217.22202845 -0.16927590

152 217.22981514 -0.16148921

153 217.23724365 -0.15406070

154 217.24433044 -0.14697391

155 217.25109124 -0.14021311

156 217.25754104 -0.13376331

157 217.26369415 -0.12761019

158 217.26956422 -0.12174013

159 217.27516427 -0.11614008

160 217.28050671 -0.11079764

161 217.28560340 -0.10570095

162 217.29046565 -0.10083870

163 217.29510423 -0.09620012

164 217.29952943 -0.09177492

165 217.30375108 -0.08755327

166 217.30777853 -0.08352582

167 217.31162072 -0.07968363

168 217.31528616 -0.07601818

169 217.31878300 -0.07252135

170 217.32211898 -0.06918537

171 217.32530151 -0.06600284

172 217.32833764 -0.06296671

173 217.33123411 -0.06007024

174 217.33399734 -0.05730701

175 217.33663346 -0.05467089

176 217.33914832 -0.05215603

177 217.34154750 -0.04975685

178 217.34383631 -0.04746803

179 217.34601984 -0.04528450

180 217.34810293 -0.04320142

181 217.35009020 -0.04121415

182 217.35198605 -0.03931830

183 217.35379469 -0.03750966

184 217.35552013 -0.03578421

185 217.35716621 -0.03413814

186 217.35873656 -0.03256779

187 217.36023468 -0.03106967

188 217.36166388 -0.02964046

189 217.36302735 -0.02827700

190 217.36432809 -0.02697626

191 217.36556900 -0.02573535

192 217.36675282 -0.02455153

193 217.36788219 -0.02342216

194 217.36895961 -0.02234474

195 217.36998747 -0.02131688

196 217.37096805 -0.02033630

197 217.37190352 -0.01940083

198 217.37279595 -0.01850839

199 217.37364734 -0.01765701

200 217.37445956 -0.01684479

201 217.37523442 -0.01606993

202 217.37597364 -0.01533071

203 217.37667885 -0.01462550

204 217.37735162 -0.01395272

205 217.37799345 -0.01331090

206 217.37860575 -0.01269860

207 217.37918989 -0.01211446

208 217.37974715 -0.01155720

209 217.38027878 -0.01102557

210 217.38078596 -0.01051839

211 217.38126980 -0.01003454

212 217.38173139 -0.00957295

213 217.38217175 -0.00913260

214 217.38259185 -0.00871250

215 217.38299262 -0.00831172

216 217.38337496 -0.00792938

217 217.38373971 -0.00756463

218 217.38408769 -0.00721666

219 217.38441965 -0.00688469

220 217.38473635 -0.00656800

221 217.38503848 -0.00626587

222 217.38532671 -0.00597764

223 217.38560168 -0.00570267

224 217.38586400 -0.00544035

225 217.38611426 -0.00519009

226 217.38635300 -0.00495135

227 217.38658076 -0.00472358

228 217.38679805 -0.00450630

229 217.38700534 -0.00429901

230 217.38720309 -0.00410125

231 217.38739175 -0.00391260

232 217.38757173 -0.00373262

233 217.38774343 -0.00356092

234 217.38790723 -0.00339711

235 217.38806350 -0.00324085

236 217.38821258 -0.00309177

237 217.38835480 -0.00294955

238 217.38849048 -0.00281387

239 217.38861992 -0.00268443

240 217.38874340 -0.00256095

241 217.38886121 -0.00244314

242 217.38897359 -0.00233076

243 217.38908080 -0.00222354

244 217.38918309 -0.00212126

245 217.38928067 -0.00202368

217.38928066546833

Solving infinite horizon dynamic models#

Value function iterations = successive approximations on the Bellman operator \(\rightarrow\) to solve for the fixed point of Bellman operator

Policy iteration method = Howard’s policy improvement algorithm, iterative solution for the fixed point of Bellman operator

Newton-Kantorovich method = Newton solver for the fixed point of Bellman operator, mathematically identical to Howard’s iterations

Convergence of infinite horizon solution methods#

In infinite horizon all solution methods continue until convergence.

How can we be sure that the algorithm would terminate?

The answer is given by the theory of contraction mappings:

Bellman operator is generally a contraction mapping

Banach theorem guarantees uniqueness of the fixed point, and

Successive approximation solver is globally convergent (works with any starting point)

Banach contraction mapping theorem (fixed point theorem)

Let \((S,\rho)\) be a complete metric space with a contraction mapping \(T: S \rightarrow S\). Then

\(T\) admits a unique fixed-point \(V^{\star} \in S\), i.e. \(T(V^{\star}) = V^{\star}\).

\(V^{\star}\) can be found by repeated application of the operator \(T\), i.e. \(T^n(V) \rightarrow V^{\star}\) as \(n\rightarrow \infty\).

In other words, the fixed point can be found by successive approximations from any starting point \(\rightarrow\) VFI method follows

What about Bellman operator?#

Bellman operator \(T: U \rightarrow U\) from functional space \(U\) to itself

metric space \((U,d_{\infty})\) with uniform/infinity/sup norm (max abs distance between functions over their domain)

Blackwell sufficient conditions for contraction

Let \(X \subseteq \mathbb{R}^n\) and \(B(x)\) be the space of bounded functions \(f: X \rightarrow \mathbb{R}\) defined on \(X\). Suppose that \(T: B(X) \rightarrow B(X)\) is an operator satisfying the following conditions:

(monotonicity) For any \(f,g \in B(X)\) and \(f(x) \le g(x)\) for all \(x\in X\) implies \(T(f)(x) \le T(g)(x)\) for all \(x\in X\),

(discounting) There exists \(\beta \in (0,1)\) such that

Then \(T\) is a contraction mapping with modulus \(\beta\).

Monotonicity of Bellman equation follows trivially due to maximization in \(T(V)(x)\)

Discounting: satisfied by elementary argument when \(\beta<1\)

Under additional boundedness conditions, Bellman operator is a contraction mapping by Blackwell sufficient conditions

\(\Rightarrow\)

unique solution

VFI algorithm is globally convergent

does not depend on the numerical implementation of the Bellman operator

Why do we need other solution algorithms?#

Although VFI is guaranteed to find the solution, it may be very inefficient when modulus of contraction (discount factor \(\beta\)) is close to one.

Newton-based method converge quadratically, but are not globally convergent, have to be initialized at their domain of attraction

Polyalgorithm would be a good idea, see NFXP in the next lecture

Inventory dynamics problem with stochastic demand in infinite time#

The model is given by the Bellman equation

Dropping the time subscripts#

Because we’ll be solving the problem in infinite horizon, the time subscripts can be dropped, and we can just have current period variables \( x,d,q,s,k \), and next period variables denoted by prime, i.e. \( x' \)

The Bellman equation is then

Bellman equation in expected value function space#

Note that similar to the bus engine replacement model, the inventory model features random variable which distribution does not depend on the previous period variables (it is idiosyncratic).

In this case it is possible to reduce the dimensionality of the fixed point problem by rewriting the Bellman operator in expected value function terms.

where the expectation is taken over the distribution of the next period demand \( d' \). The conditioning on \( x,d,q \) can be dropped exactly because \( d' \) is idiosyncratic.

We can then write the Bellman equation as

Taking the expectation with respect to \( d \) on both sides, we get

By assumption the inventory is discrete, and so it is natural to assume that the demand is also represented as a discrete random variable. Then the expectation can be written as a sum weighted with the corresponding probabilities \( pr(d) \), as

This is functional equation in \( EV \) which is also a contraction mapping!

Origin of the term Dynamic Programming#

The 1950’s were not good years for mathematical research. We had a very interesting gentleman in Washington named Wilson. He was Secretary of Defence, and he actually had a pathological fear and hatred of the word “research”. I’m not using the term lightly; I’m using it precisely. His face would suffuse, he would turn red, and he would get violent if people used the term, research, in his presence. You can imagine how he felt, then, about the term, mathematical. Hence, I felt I had to do something to shield Wilson and the Air Force from the fact that I was really doing mathematics inside the RAND Corporation.

What title, what name, could I choose?

In the first place, I was interested in planning, in decision-making, in thinking. But planning, is not a good word for various reasons. I decided therefore to use the word, “programming”. I wanted to get across the idea that this was dynamic, this was multistage, this was time-varying.

I thought, let’s kill two birds with one stone. Let’s take a word which has an absolutely precise meaning, namely dynamic, in the classical physical sense. It also has a very interesting property as an adjective, and that is it’s impossible to use the word, dynamic, in the pejorative sense.

Thus, I thought dynamic programming was a good name. It was something not even a Congressman could object to. So I used it as an umbrella for my activities.

— 📖 Bellman’s autobiography “The Eye of the Hurricane”

References and Additional Resources

📖 Rust [2016] “Dynamic programming”, The New Palgrave Dictionary of Economics

📖 Adda and Cooper [2023], “Dynamic Economics: Quantitative Methods and Applications”, chapters 2 and 3

📖 Aguirregabiria and Mira [2010] “Dynamic discrete choice structural models: A survey”

Wiki: Bellman equation https://en.wikipedia.org/wiki/Bellman_equation

Computer science view on DP link

“Knowing When to Stop” by Theodore Hill, American Scientist link